Fixed Deposits, or FDs, have been the go-to investment choice of many. FDs have been a safe and default choice for both individuals and corporates. And this is primarily because they offer assured returns and are latent to the vagaries of the market. The recent hike in FD rates from different banks following RBI hiking repo rate (the rate at which the apex bank lends to commercial banks) have made them further lucrative.

However, as we step into 2023, with inflation showing little signs of ebbing, it’s imperative for you to step outside the comfort of FDs and look at better alternatives, like debt mutual funds. Let’s see why.

Real Returns from FDs May be in the Negative Territory

Though fixed deposit interests have recently gone north, the real returns from FDs are muted. Real returns are returns you earn after accounting for taxes and inflation.

Real Returns = Interest Earned – (Taxes + Inflation)

Note that returns from FDs are fully taxable. The interest earned is added to your income and taxed as per your tax slab. If you are in the 30% tax bracket, the 7% interest on FDs gets reduced to less than 5%. This effectively brings returns from FDs in the negative territory given that consumer inflation stood at 5.88% in November 2022. That’s not all.

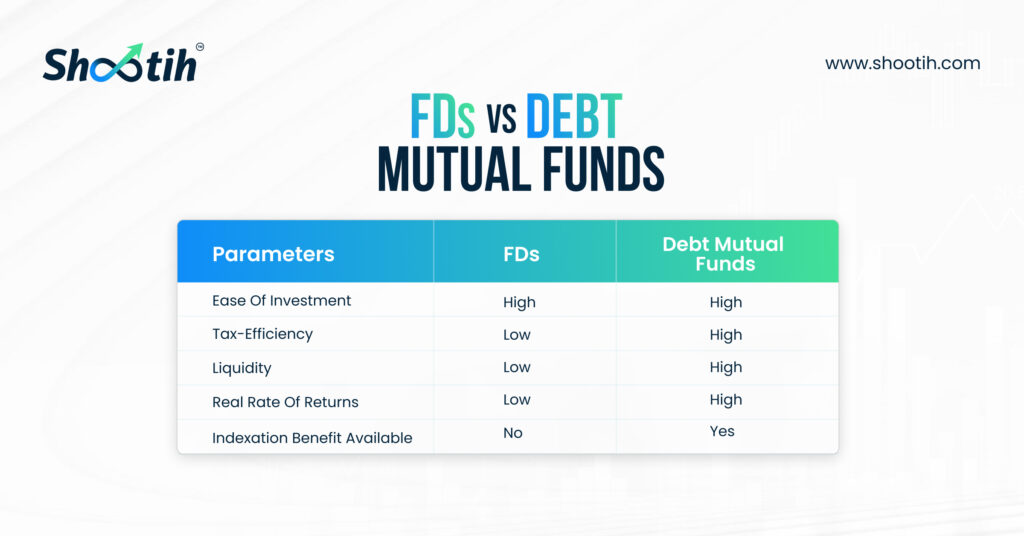

FDs don’t enjoy the indexation benefit of debt mutual funds, which you get if you hold the latter for more than 3 years. Indexation adjusts the purchase price of the as per inflation, which effectively lowers gains and reduces taxes in the process.

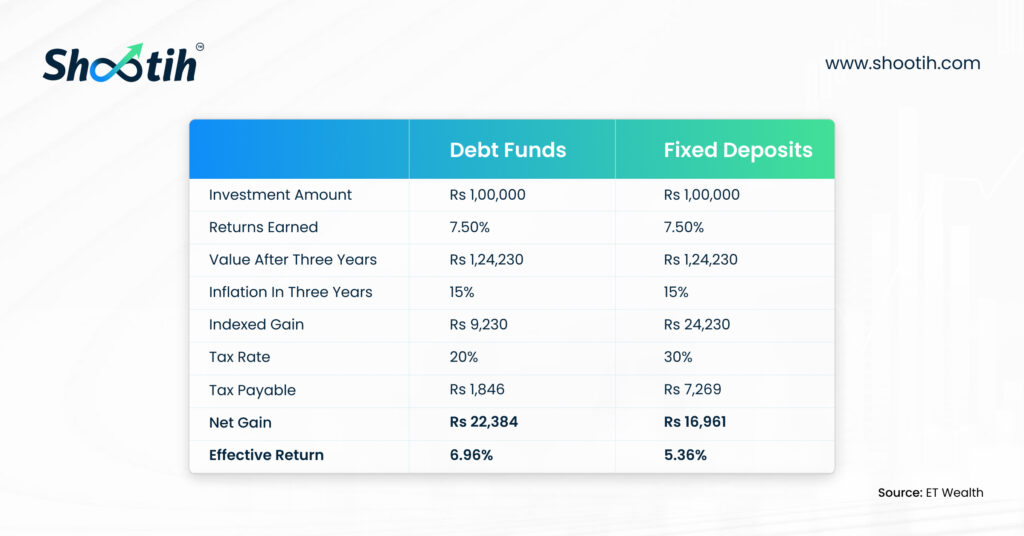

Suppose you had invested Rs. 1 lakh in a debt fund 3 years ago, which gave 7.5% compounded returns. If the cost of the inflation index rose to 15% in three years, the purchase price of the fund is raised to Rs. 1.15 lakhs, thus reducing the gains and tax. However, FDs don’t enjoy this benefit which enhances your tax outgo (see image below).

Greater Liquidity With Debt Mutual Funds

This is another aspect where debt mutual funds score high over fixed deposits. If you want to liquidate your FD before tenure, you not only need to pay a penalty, but also withdraw the entire amount. However, with debt funds, you can make partial withdrawals as per your needs.

Also, there are more than 10 types of debt mutual funds that you can choose from to invest as per your goals and risk appetite.

Summing Up

If you are looking to invest business money for growth, debt mutual funds can be a better alternative. With inflation here to stay, investing in debt mutual funds can yield productive results in the long run and ensure you grow your business wealth in a disciplined and sustained manner.

Feeling difficulty in selecting the right investment option for investing your money? Book a call with our experts and get free assistance for corporate investments.

Disclaimer: Mutual fund investments are subject to market risks, please read all scheme-related documents carefully

The content of this blog is not intended to serve any professional advice or guidance and Shootih takes no responsibility or liability in whatsoever manner for any investment decisions made by the readers of this blog or other blogs. Readers should seek independent professional advice before making any investment decision based on the information provided on this website.